The VA loan is one of the most powerful home buying tools available to those who qualify. A few benefits of the VA home loan are an option for ZERO down payment, no Private Mortgage Insurance, and lenient credit qualifications.

There are specific criteria to qualify for the VA home loan, one of which is the Minimum Service Requirement. This is essentially a baseline for service qualifications.

The Minimum Service Requirements for The Army, Navy, Air Force, & The Marine Corps:

Served 90 consecutive days of active service during wartime.

Served 181 days of active service during peacetime.

Recently, the VA has revised their qualifications for those who serve and have served in the National Guard, which has opened the VA loan to thousands of National Guard members.

National Guard updated VA Loan qualifications are as follows:

If you’ve served for at least 90 days (minimum 30 consecutive days) of active duty under Title 32 orders, you meet the minimum service requirement.

Over recent years, thousands of National Guard members were activated under Title 32 Orders, meaning many of them are eligible for a VA Home Loan.

Have you served or are currently serving in the National Guard? Reach out to one of our branches today to learn about the VA home loan and find out if you are eligible today!

Get Your COE!

At Benchmark, we are dedicated to serving veteran clients and providing them with a world class home buying experience. We have changed the way VA lending is done. That is why Benchmark never quits.

Contact your local Benchmark branch. Contact us today for personalized information. Call me yourself or request a call from me. WeI would be honored to provide you with our famous excellent service for your new loan.

With mortgage interest rates at a level not seen for over a decade (see chart below), the question of whether to wait for interest rates to fall is creeping in. This is not unreasonable, however, it does beg the question.

Are rates actually high?

If you take a look at the chart below, you can get a pretty good idea. At first glance, you may be tempted to think, “With rates THIS high, they’re bound to come back down before too long.” You may think this looks like an economic blip; that things will calm down back to normal soon.

But a longer view may give you a different perspective.

Looking over the past ten years means we are looking back on a housing market recovering from the 2008 crash (the conditions of which do not exist today). This is a short-term view; A view that includes a lot of market manipulation intended to encourage buying through various means, including keeping interest rates low.

To see more clearly, we need to take a look at a much longer time frame.

The longer view gives a sobering realization. Current rates do not appear to be high at all, in the long term. The reality is that the lower rates we’ve been experiencing are a strange occurrence, fueled by quantitative easing. The rising rates we see now are the result of a slight reversal of this practice. To better understand what this really means, take a look at the chart of the Federal Reserve’s Balance Sheet over the last 10 years below.

The Federal Reserve was buying investment securities (including mortgage debt securities) to help prop up the economy, and to bring mortgage interest rates down. The fact that the strategy worked is a clear sign that its reversal means that rates have, and will probably continue to drift back up to natural market levels. As we have discussed before, a rising interest rate means a rising cost of homeownership.

However, it’s clear that interest rates are not the only thing going up.

Inflation is a value killer

Inflation is on everyone’s minds as of writing. The Consumer Price Index shows a fairly sharp climb since the COVID-19 pandemic began, and the Federal Reserve’s increase in interest rates (not the same as mortgage interest rates) was intended to alleviate inflation. Oh, you want a chart to show inflation? See below.

The rising prices means that your money is worth less. Everything costs more than it did, which can eat into what you can afford for a monthly mortgage payment. It may seem like a good idea to wait: for your money to be worth more, for the economy to stabilize, and for mortgage interest rates to return to their senses.

As discussed previously, however, there is no solid basis for anticipating mortgage rates to come down any time soon, if at all. If this is true, though, does it even make sense to buy a home? Is real estate really the right place to put your money if the cost of living goes up?

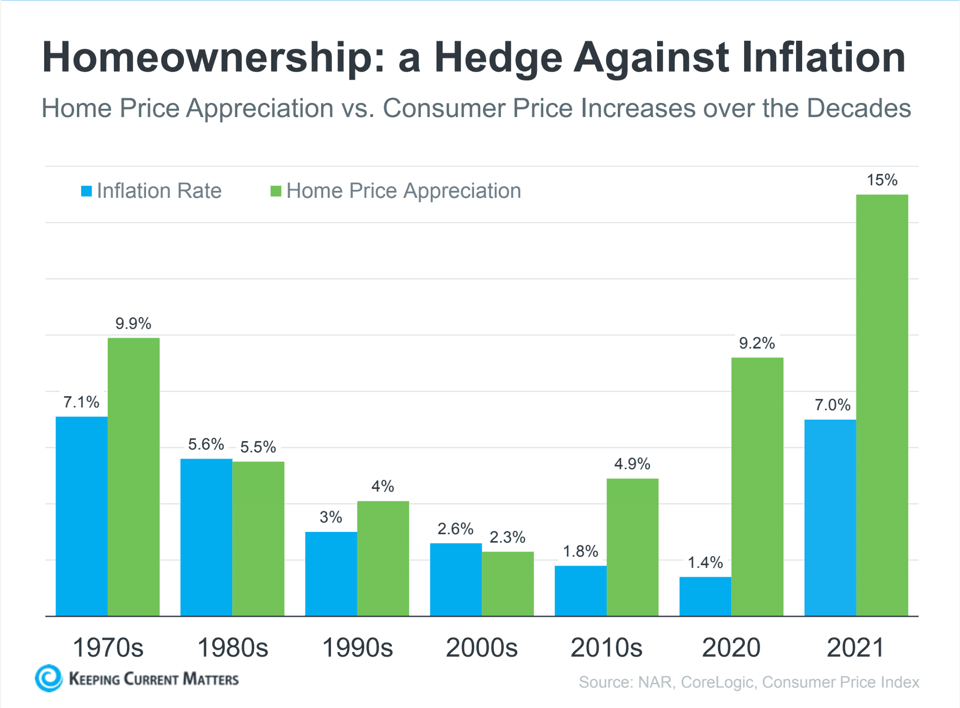

Rising prices mean cash held in hand is losing value, while investments that rise with it are, at the very least, holding value.

“Real estate is one of the time-honored inflation hedges. It’s a tangible asset, and those tend to hold their value when inflation reigns, unlike paper assets. More specifically, as prices rise, so do property values.”

Mark Cussen, Financial writer at Investopedia

Higher cost (rates) means less competition

We have seen a cooling of demand in the housing market since rates have started rising. The sellers’ market has become more equitable, favoring buyers in many locations. There have been fewer multiple-offer scenarios, and even when there are multiple-offers, there have been fewer offers to compete with.

If you live in a competitive market, Benchmark can give you an edge. If you don’t live in a competitive market, this could be your opportunity to get your offer accepted on the best possible terms. Again, this is what we do best. Contact us get more information about how you can win with Benchmark.

Housing prices tend to climb

The financial world is full of commonly repeated advice. Invest early and invest often. The best time to plant a tree is 20 years ago; the second best time is today. Add this one to the list: Buy now to buy more.

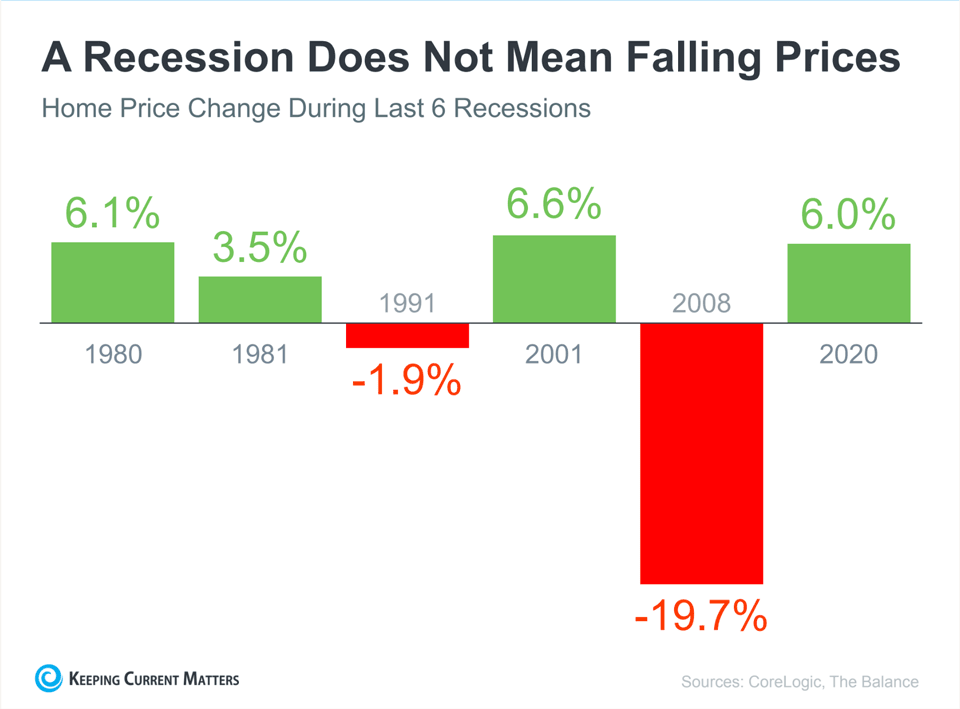

Even if we find ourselves in a recession, as some predict, this does not guarantee falling home prices. The exception being the notorious 2008 recession due to the collapse of real estate debt-based investment schemes, the conditions of which do not exist, and have not existed since.

There is no indication that they will come down any time soon. Even if you do suspect that rates will be reduced in the future, you should weigh the cost of waiting. Of course, you may be able to refinance at a lower rate in the future, while taking advantage of current home prices now.

Either way, your rent payment will become at least a partial investment into a physical asset you own. The principal portion of a mortgage payment directly reduces the amount you owe on your home. When you pay rent, the only equity you are building is your landlord’s.

The chart above is not plotting rent prices. The chart is plotting rent price inflation. See the dip caused by the COVID-19 pandemic starting early 2020? This isn’t really a dip; it’s just a reduction in the annual inflation rate of rent prices. Inflation never reversed within the last decade.

How do you escape the squeeze?

It would do no good to lie to you and tell you that there is an easy way out of the rising cost of housing. We have published a short list on How to Get Ahead When You Can’t Get the House You Want, but the wisest words I’ve ever read on housing were these: “Welcome to California. Buy a house immediately.” This is less about California, and more about how to live with rising housing prices. This was advice given to someone who moved there for a job in the tech industry. The advice holds true now: the sooner you buy, the better your chances of being able to buy.

If you think you might want to become a homeowner, I encourage you to contact us. Even if you think you cannot afford a home yet, or if you don’t know what you need to do to get started, we specialize in helping people just like you achieve the American dream of homeownership. Benchmark has been helping people get into their own home since 1999, and we’ve learned a few things along the way.

Contact your local Benchmark branch. Contact us today for personalized information. Call me yourself or request a call from me. WeI would be honored to provide you with our famous excellent service for your new loan.

Housing inventory is one of the factors that can dramatically affect the temperature of the real estate market. Less inventory means potentially more competition and higher prices. Whether you’re a buyer or currently in the seller market, this can determine your strategy. Like most investments or assets, housing inventory can fluctuate anytime. This is why it’s important to gauge your options before buying a property.

Quick Update: Real Estate Industry Trend

Despite the ongoing economic challenges, housing prices continue to rise. This just shows the resilience of the real estate industry. As many experts have predicted, home buying and selling prospects have significantly improved in September 2020 from pandemic lows. Homebuyers are moving much faster than this time last year. According to the forecast, this upward trend could continue for three to five years.

Low Mortgage Rates: Biggest Factor in Today’s Housing Inventory Shortage!

According to an article recently published by Business Insider, low mortgage rates are one of the main reasons for the current housing inventory shortage. Several reports also show that a house is the hottest “pandemic purchase” in the country.

Today, property investors, realtors, and even casual homebuyers are now on the hunt for the best deals they can get. This makes it more challenging for buyers to find a property that suits their budget and needs.

Let’s have a look at these key takeaways:

Residential properties have become a valuable asset, as more and more Americans take advantage of low mortgage rates.

Existing home sales continue to surge forward for the last 3 months since the real estate market reopened from the shutdown. It soared to a 14-year high in the previous two months. There are also reports of upcoming home sales.

Experts’ forecasts revealed that the country may experience a housing inventory shortage for the next coming years. There are new residential property projects, but not enough to keep up with the demand.

Other Important Predictions From Industry Experts

Buying a house is a big investment. Whether you’re doing this for personal reasons or as a future investment, it’s always better to keep learning about the real estate market. A good way to do this is to consider investors’ expert opinions. Here are some forecasts for the real estate market from several experts:

The demand for refinancing and housing loans remains at large

The high demand for refinance and housing loans has raised the competition among realtors, property managers, and lending officers. Many mortgage organizations, particularly new companies may have a hard time competing. Potential buyers may also experience some delays with loan applications.

Homebuyers need to explore more options when purchasing properties

Due to the housing inventory shortage, homebuyers need to exert more effort when looking for prospect properties. Be resourceful. You might want to check out some auctions, foreclosures, short sales, and bank-owned properties.

Location will still be one of the keys

Homeowners are adapting to a new lifestyle due to the current pandemic state. However, due to this upward trend and housing inventory shortage, it may be difficult for homebuyers to find the perfect home for themselves or their families.

The rise of new mortgage company startups and lending officers

Despite the global crisis, the US housing industry still looks solid,. This means many investors may be looking for opportunities to join the bandwagon, so don’t be surprised if there are more mortgage organizations in a few months or so.

Notable Reminders for Homebuyers

Although now is a good time to buy a house or invest in a property, the entire process can be a lot more challenging due to the housing inventory shortage. As a homebuyer, it’s important to find a trusted mortgage broker or loan officer. These professionals can help simplify the process for you. Just make sure to choose loan officers with several years of industry experience.

Benchmark is one of the leading mortgage companies in the United States. For more than two decades, we have helped our clients find the right loans and manage their mortgage needs. We have seasoned mortgage consultants in over 80 branches nationwide, ready to discuss the best home buying options that suit your budget and needs. Through the years, we’ve been delivering excellent customer service, by providing competitive rates and the most efficient loan processing!

So, if you’re looking for an expert loan officer you can trust, send your loan application today!

What do you do when you move away in process of buying a home during a worldwide pandemic, finding yourself in a hotel which you can't leave? Benchmark never quits.

Have you told yourself that you’re too _____ to buy a home? The blank could be almost anything. Whether you think you’re too broke, too poor, or your credit score is too low, are you allowing an invisible script to prevent you from attaining your dream of owning your own home?

You don’t have to be rich. You don’t have to have a 750+ credit score. You don’t need $50,000 in savings. Don’t believe me? Sit back, grab a cold drink, and hear me out.

Big Down Payments Are Old Hat

If you can scrounge up ~$10k for a down payment, I wager that you can probably buy a home. It’s not a sure thing, of course, but hear me out. While a 20% down payment is excellent wisdom, it isn’t a requirement. Depending on the loan type, and where you buy, you could be required to pay less than 5% down to get into it. FHA loans require 3.5% down, which is less than $10k, assuming the median sales price of $248,867*. There are some conventional loans that require as little as 3% down. That’s ~$7,500, assuming a sales price of $248,867.

Let’s assume you don’t have the full ten grand lying around in a checking or savings account. Some, or even all, of your down payment can come from gifts from family, depending on certain restrictions. The point is that you maybe shouldn’t let your savings dictate your eligibility. Even if you haven’t been prioritizing your savings, how long do you think it would take to save up? I don’t pretend to know or understand your financial situation, but it may come down to something as simple as organizing your priorities.

* https://www.zillow.com/home-values/

Your Credit Is Probably Fine

The average FICO credit score in the United States as of September 10, 2019 was 706**. In fact, as of January 13 of this year, 59% of people in the US have a FICO credit score greater than 700, and only 18% have a credit score that is considered subprime***. For everyone else, there is probably a mortgage product or program that suits your needs. I don’t pretend to know you or to know about your finances, so take that with a grain of salt. None of this is a guarantee, but I’m guessing based on averages.

Even if your credit isn’t where you want it to be yet, there are such things a conditional approvals. To learn more about this, it’s best to contact a mortgage pro. I might have a suggestion about how to find one at the end of this article.

The total balance of your personal debt isn’t a very important factor in qualifying for a new home loan. Once again, I don’t pretend to have a clue about your personal finances, so forgive the section title. Your debt balance is important, but probably not when it comes to buying a home.

If you are worried about your student loan debt, don’t be. This kind of debt is a little more complicated, but it can be based on your monthly minimum due or 5% of the balanced divided by 12 months, unless you’re in deferment for more than a year past the closing date. Like I said, it’s complicated, but it’s probably not preventing you from buying a home. The only way to find out how your particular student loan arrangement affects your ability to buy a home is to talk to a mortgage pro. Don’t worry, we’ll get to that soon.

If you have any other kind of personal debt, only the minimum payment as listed on your credit report matters. No matter your debt, this is what you need to know. The equation is called the “debt to income” ratio, or DTI. This is a ratio of your monthly financial debt obligations and your monthly income. That helps determine how much house you can afford, when coupled with your down payment and creditworthiness.

Asking Never Hurt Anyone

If you dream of owning your own home, like I once did, the only way to really know what your options are is to talk to a mortgage pro. If you only remember one tip from this short article, this is it. Nervous? I understand. So do the pros here at Benchmark.

Even if the answer is “not yet”, you’ve made the first step towards achieving your dream, and your Benchmark loan originatorwemy team will be with you every step of the way.

The current market is not the same one that existed only three months ago. Open houses are not as “open” as they were, and COVID 19 has impacted every aspect of the real estate market. We got with JD Tomlin, a realtor with the JD Tomlin Team (est. 2010) in the DFW area, to discuss some of the hottest issues that have come up with the changing industry.

The team you work with matters! The industry has changed a lot, and working with an expert who can navigate the changing guidelines is more important than ever. Lenders today are dealing with constraints that have taxed the entire industry with challenges, including long wait times on appraisals. In some cases, some lenders are just not sending funds to close their loans. Ultimately, how long is the home buying process taking? Overall, transaction times haven’t changed very much. Benchmark has a team dedicated to making sure loans close quickly, efficiently, and on time. Read more

Home inventory helps predict whether it’s a “Seller’s Market” or a “Buyer’s Market.” When there are too many houses for sale, the buyer has the advantage. When there are not enough houses, sellers have the advantage. Home inventory changes based on location, so good advice in one city, may be harmful in another. No matter what inventory level your area is seeing, the important thing to note is that houses are still selling, people are still moving, and you can too! Ask your local Benchmark Loan Officer to connect you with one of their trusted realtor partners to get started today! Read more

If you are considering listing your house for sale, you have probably considered the fact that people will want to come tour the inside of the house. This is where the realtor you choose can make a big difference. Photographs and 3D digital tours have become popular solutions to boosting your house listing, and allow potential buyers to see enough of the house that they may make an offer, site unseen. Realtors are also seeing that every protective measure is taken to make sure they enter a house with facemasks and sanitization before, and after, viewing a house. Read more

It’s no secret that realtors work hard to create a great home finding process for their clients. For top notch realtors, this has not really changed. Restrictions have been put in place to ensure that visiting homes is done safely, and inline with the CDC’s recommendations. When home sellers have multiple people wanting to look at the house, Realtors will often try to access the house without their clients, providing a walk-through video, as well taking note of things the homebuyer may want to know about. This requires a lot of trust in your realtor partner, and borrowers may need to be ready to potentially purchase a house without actually stepping foot inside of it. Read more

It’s no secret that realtors work hard to create a great home finding process for their clients. For top notch realtors, this has not really changed. Restrictions have been put in place to ensure that visiting homes is done safely, and inline with the CDC’s recommendations. When home sellers have multiple people wanting to look at the house, Realtors will often try to access the house without their clients, providing a walk-through video, as well taking note of things the homebuyer may want to know about. This requires a lot of trust in your realtor partner, and borrowers may need to be ready to potentially purchase a house without actually stepping foot inside of it.

Home inventory helps predict whether it’s a “Seller’s Market” or a “Buyer’s Market.” When there are too many houses for sale, the buyer has the advantage. When there are not enough houses, sellers have the advantage. Home inventory changes based on location, so good advice in one city, may be harmful in another. No matter what inventory level your area is seeing, the important thing to note is that houses are still selling, people are still moving, and you can too! Ask your local Benchmark Loan Officer to connect you with one of their trusted realtor partners to get started today!

The team you work with matters! The industry has changed a lot, and working with an expert who can navigate the changing guidelines is more important than ever. Lenders today are dealing with constraints that have taxed the entire industry with challenges, including long wait times on appraisals. In some cases, some lenders are just not sending funds to close their loans. Ultimately, how long is the home buying process taking? Overall, transaction times haven’t changed very much. Benchmark has a team dedicated to making sure loans close quickly, efficiently, and on time.

If you are looking for your first, or next, home, you will likely tour several before finding "the one." Before you let yourself be swept off your feet, stay grounded and take a closer look. While you will want to get a professional inspection, it's a good idea to get a good idea on your own. Doing so may save the cost of a professional, if significant issues are discovered, or if the home needs more work than you are willing to take on.