COVID-19, the Federal Reserve cuts rates, and Rate locks now good for 60 days. A lot is going on in the housing market and the country as a whole. Let's dive in, and see how this could affect you and your mortgage.

COVID-19, the Federal Reserve cuts rates, and Rate locks now good for 60 days. A lot is going on in the housing market and the country as a whole. Let's dive in, and see how this could affect you and your mortgage.

In this video, Jim McMahan, President of Benchmark Mortgage, talks about the market, interest rates, and debt strategy to help you decide whether refinancing might be a good option for your financial goals.

In 2017, Australian millionaire Tim Gurner famously attempted to blame millennial homebuyer obstacles on their inability to avoid frivolous spending on $19 avocado toast, in comments that were widely mocked throughout the internet.

Many commentators are still quick to point the finger at extravagant spending to explain why homeownership among younger adults has declined compared to previous generations. However, the more likely culprit is soaring student loan debt and a limited supply of homes causing rapidly inflating prices, which is making it more difficult for millennials to afford homes.

Despite what you hear, it’s not all doom and gloom for aspiring millennial homebuyers. According to the National Association of Realtors (NAR) latest study, millennials continue to be the largest generational cohort of buyers, making up 36% of the purchase market.

Check out the latest statistics and trends among this influential bloc of homebuyers.

Many people still think of millennials as teenagers, instead of young adults in their 20’s and 30’s who currently make up the largest generation in the workforce. NAR’s study defines millennials as buyers age 20-37.

Of this group:

After analyzing their demographics and buying habits, it is clear that millennial buyers have become a powerful force in the housing market. As it turns out, avocado toast is not preventing millennials from buying homes.

The Mortgage Bankers Association reported a 4.1% increase in mortgage applications from the prior week.

Steve Remington, Benchmark’s Chief Operations Officer, noted that the increase in applications could be a consumer response to the recent trend in the market, indicating a shift from the prolonged period of low interest rates.

“Mortgage Bankers Association Data indicates a slight uptick in refinances for people who might be trying to take advantage of these lower interest rates. We don’t foresee doom and gloom with rates skyrocketing, but we do see an upward pressure of interest rates in the short term,” says Mr. Remington.

He also suggests that people in the process of building a home, or looking to build a home, may wish to consider looking at options to lock in their interest rates early. “If you are building a house and it takes 6-12 months to build, you might consider seeking a long-term lock option that Benchmark may be able to offer.”

You can read the full report from the Mortgage Bankers Association here.

Last year, the conforming loan limit was set to increased to $424,100 for this year (2017). Now, most of the United States will see an increase for single unit properties to $453,100 for 2018.

The HERA (Housing and Economic Recovery Act) indicates that the baseline conforming loan limit should be adjusted with the change in the average home price in the United States every year.

According to the FHFA (Federal Housing Finance Agency):

According to FHFA’s seasonally adjusted, expanded-data HPI, house prices increased 6.8 percent, on average, between the third quarters of 2016 and 2017. Therefore, the baseline maximum conforming loan limit in 2018 will increase by the same percentage.

A loan is considered “conforming” when it conforms to Government-Sponsored Enterprise (Fannie Mae and Freddie Mac) guidelines.

In light of the recent announcement of the S&P CoreLogic Case-Shiller Home Price NSA Index increase from last year, and FHFA’s seasonally adjusted, expanded-data HPI increase, this conforming loan limit adjustment is a welcome change for home buyers in high valuation markets.

To learn more about this increase, you can read the press release from the FHFA by going to https://www.fhfa.gov/Media/PublicAffairs/Pages/FHFA-Announces-Maximum-Conforming-Loan-Limits-for-2018.aspx.

Source: September S&P CoreLogic Case-Shiller National Home Price NSA Index Up 6.2% In Last 12 Months

Recent Analysis of the September HPI figure show as a 6.2% annual gain in home prices, up 5.9% from the previous month. Several large markets that were hit hardest in the financial crisis are reporting the highest gains, including San Diego (up 8.2%). 15 of the 20 major cities posted increases before seasonal adjustments, but all 20 reported increases after seasonal adjustments.

On the bright side, these price increases continue to be fueled by a strong economy, low mortgage interest rates, and a low inventory of homes; however, continued price increases and low inventories can put pressure on affordability for some people.

Steve Remington

Chief Operations Officer at Benchmark

Calling it “Dynamic Ads for Real Estate,” Facebook describes the service,

Facebook’s dynamic ads for real estate leverage cross-device intent signals to automatically promote relevant listings from your inventory with a unique creative on Facebook.

This is the first time the social media giant has ventured into Real Estate specific advertising, raising potential concern for platforms specializing in the niche industry. With this move, Facebook offers direct advertising access to real estate professionals who can now show relevant properties to a target audience on a platform that they already use.

Benchmark’s own Marketing Director had this to say,

Facebook entering the real estate space is huge for the every day Realtor. They will now have the ability to reach targeted, potential buyers with accurate information that comes straight from the listing agent as the source. – Garrett Finkelstein

Whether this poses a threat to existing niche vertical advertising platforms remains to be seen, but one thing is for certain: the advertising landscape is changing at Facebook.com.

With more Millennials interesting in buying homes, this comes across as a step towards reaching the audience where they are, in a way that is automatically optimized for both advertiser and customer alike.

The Rate of Homeownership has increased from 34.3% to 35.3% from first Quarter 2017 to Second Quarter 2017 for those under 35 years of age, according to a report from the United States Census Bureau.

While popular media seems to portray Millennials as a generation of renters, a whitepaper from First American lists six reasons why the number of Millennials becoming homeowners will continue to rise. Here is a quick summary.

First American says,

“Our model shows that, all other factors being equal, the likelihood of homeownership increases by 3 percent for those that earn a bachelor’s degree over those with a high school degree. The likelihood of homeownership jumps another 3 percent for those that earn a graduate degree.”

To summarize, more education results in a higher rate of homeownership. Since Millennials are the most educated generation in the United States, we should expect to see the rate of homeownership for this group increase over time.

As a generation known for delaying life milestones, many are marrying later. With the homeownership rate being 30% higher for married couples over non-married homes (according to First American), we can expect to see the rate of homeownership increase over time for Millennials.

According to First American‘s research:

“The homeownership rate is 1.7% higher for households with one or two children compared to households with no children, and it is 5.4 percent higher for households with three or more children.”

As Millennials mature, there may be an increase not only in marriage, but also in producing the next generation. According to First American‘s latest report, this could also result in a bump in homeownership for this up and coming group.

First American‘s study ties recent gains in income growth and a stronger economy to an increased willingness and ability to buy a home. While this is referring to the entire labor pool, it includes Millennials.

This is hardly proof, but it is interesting to note that ages 25-34 is the largest age group represented in visitors to Benchmark.us so far in 2017, at 32% of all sessions being within this age range.

The generations are aging, expectations are changing, and the time is right for the Millennials to take on the American Dream of Homeownership and to establish familial wealth.

Most agree that home prices have risen, and are still on the rise. We have written about why this is not like the housing bubble that we saw nearly ten years ago. In some areas, there are not enough homes for sale to meet the demands of home buyers, and prices are driven up organically. see – Low Housing Inventory Driving Values Up – Benchmark

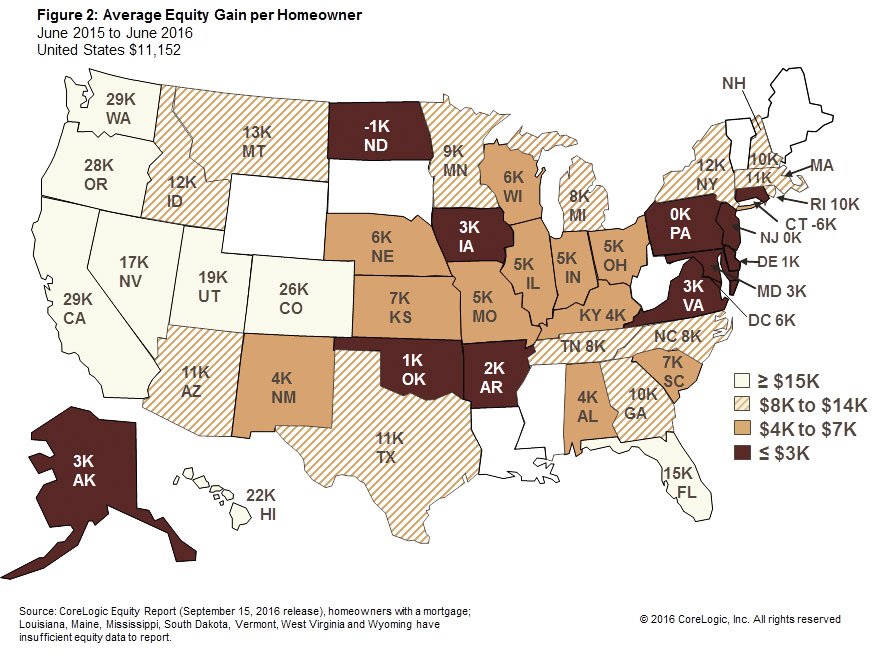

While this can make things more difficult for some home buyers, there is a bright side. The average household in the US gained over $11,000 in equity in the last year owing, at least in part, to rising home values, according to CoreLogic’s most recent US Economic Outlook.

This map is originally provided by CoreLogic’s report. This shows the average, by state, of home equity gained per homeowner from June 2015 to June 2016. The national average equity gain per homeowner was $11,152.

To address any fears that this nationwide appreciation harkens back to the bubble burst a decade ago, please recognize that homeowners are investing this new equity in their homes and in themselves rather than in speculation or assets subject to standard depreciation.

What does this mean? This means that it is probably helping families to pay for college, start small businesses, pay off their mortgage faster, or moving to a home more suited to their dreams or lifestyle.

CoreLogic’s predictions are that home prices will rise another 5% by this date in 2017. Would you believe that it is still cheaper to buy than to rent? Stay tuned for our next post!

CNBC published an article on their Real Estate blog entitled, “‘Massive’ shortage of appraisers causing home sales delays”

Below are a few quotes that summarize the story quickly, in case you don’t have the time or patience to read the article yourself.

“The appraisal shortage is massive. You’re seeing significant delays, you’re seeing cost increases, you’re seeing rate [locks] expire,” said Brian Coester, CEO of Rockville, Maryland-based CoesterVMS, a national appraisal management company.

…when the U.S. housing market came crashing down, the number of appraisers has shrunk by 22 percent, according to the Appraisal Institute, an industry association. With so few new cadets, the current population of appraisers is aging. More than 60 percent are over the age of 50.

…the decline in new appraisers is largely due to new regulations…

…appraisers no longer see a need to pay apprentices, but at the same time, licensing requirements to become an appraiser include 2,500 hours of appraisal experience to be completed in two years as an apprentice.

In some of the nation’s hottest housing markets, where sales are up double digits compared to a year ago, the shortage means searching far and wide for an appraiser.

[Home] Prices could change in the course of two months, the delay time it is now taking in some markets to have an appraisal done. Mortgage rates are also starting to move in a wider range, and that makes rate-locks ever more important.

read more: http://www.cnbc.com/2016/09/27/massive-shortage-in-appraisers-causing-home-sales-delays.html

Our 5 Core Values have served us well. We believe that they will continue to enable us to thrive, even in a complicated market.

We built our reputation and our business on these Core Values, one of which is Relationship. Another complimentary value that we hold dear is Positive Attitude. The combination of these can go a long way in ways you may never expect. So what is our approach?

To be as clear and transparent as possible in building relationships with partners in helping our mutual clients to get their new home as smoothly as possible. Just like we pride ourselves on being thorough and courteous for our clients, we strive to be open and thorough in our communications with partners.

We have an experienced staff who search daily to ensure coverage. We foster a positive relationship with our panel of appraisers.

Our appraisers prioritize us because we pay them generously and pay them quickly.

We have an advantage over appraisal management companies, as our appraisers receive the full fee, rather than just a percentage, and we have control over both the fee and the due date.

We have clear channels of communications with our appraisal department to quickly and efficiently resolve disputes and revisions.

For years, we have made the mortgage process look easy to those who have entrusted us with their home loans.

…efficiency and customer service is second to none.

Tom and his team make you feel like family and not just a number. He walks you thru all of your options and helps guide you thru the whole process. The attention he gives to his clients is untouchable. You will not get service like you get from him anywhere. 5 star all the way

…the Benchmark Mortgage Team are outstanding! From start to finish they kept us informed of the process, progress, and approvals. By far the most professional and expedient loan process I have ever been through.

We take service seriously. These are just a taste from a small collection of genuine testimonials giving by our Benchmark clients/fans. I encourage you to view more testimonialsmy testimonials. If you love being taken care of and like what you see, call mefind your branch or apply now