Now, you could get a refinance loan for any term between 15 and 30 years! Get a better rate without "starting over". Benchmark presents: Odd Term Mortgages.

Now, you could get a refinance loan for any term between 15 and 30 years! Get a better rate without "starting over". Benchmark presents: Odd Term Mortgages.

Yesterday, December 7, 2017, the Federal Housing Administration announced that for 2018, 3,011 out of 3,141 counties in the U.S. (~96% of all counties in the nation) will see an increase in FHA loan limits.

Ceilings and Floors

In high-cost areas, the FHA’s loan limit ceiling will increase this year to $679,650, up from $636,150, providing a $43,500 increase. In addition, the floor will rise from $275,665 to $294,515, an $18,850 increase.

Reverse Mortgages

The National Mortgage Limit for FHA-insured Home Equity Conversion Mortgages, or reverse mortgages, will also rise with the loan limit ceiling from $636,150 to $679,650, for an $18,850 increase.

Next Year

FHA case numbers assigned on Jan. 1, 2018 or later will be subject to the new loan limits.

HUD’s Press Release: https://www.hud.gov/press/press_releases_media_advisories/2017/HUDNo_17-110

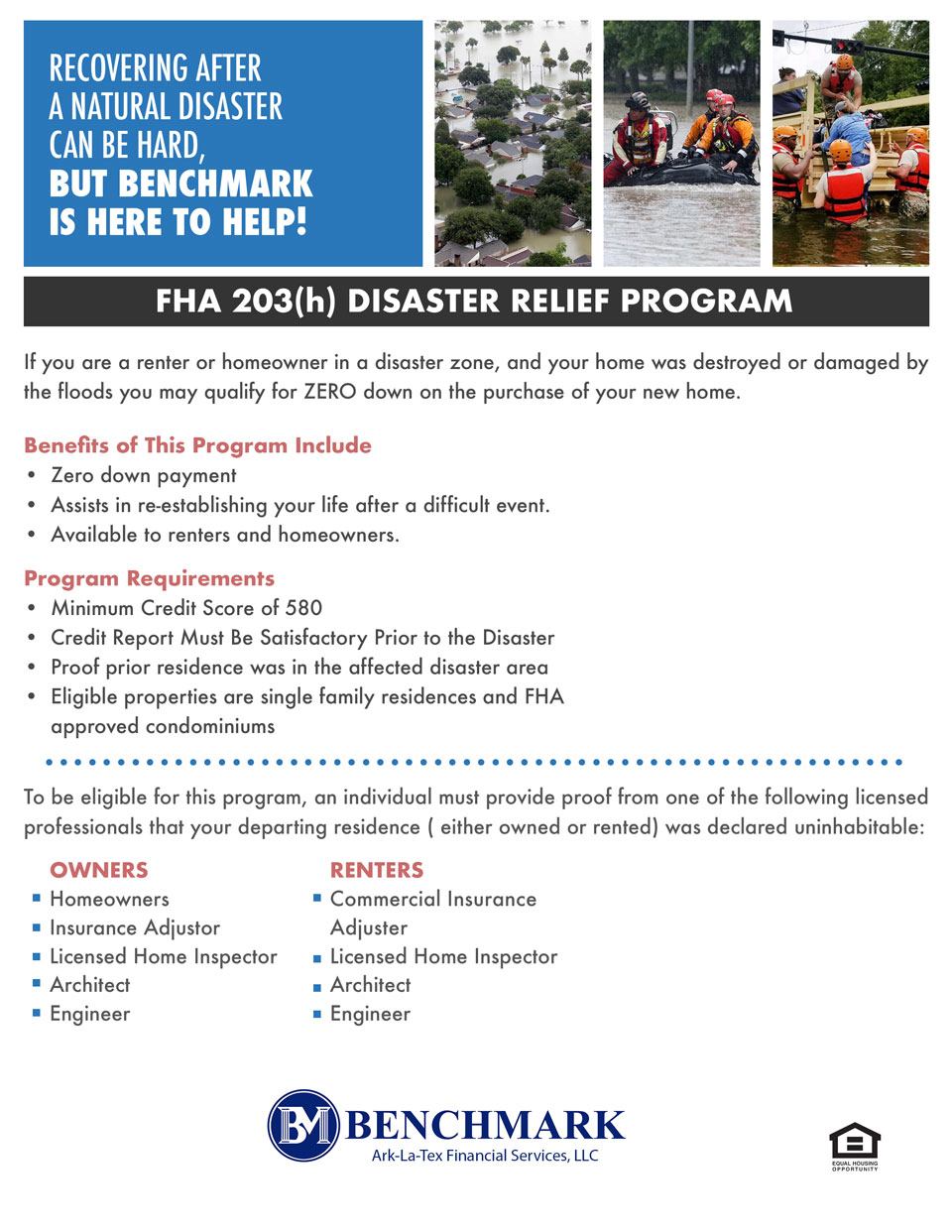

In the aftermath of the historic flooding in South Texas, and in anticipation of Hurricane Irma in the Caribbean, you should be aware of your financial options in the wake of devastation.

The FHA 203(h) is a ZERO down program, and is available to homeowners and renters alike.

At Benchmark, we know how important it is to rebuild after devastation. Your Benchmark Loan Originator can help with options like the FHA 203(h) program.

[UPDATE – According to Housing Wire, This reduction has been indefinitely suspended mere minutes after Donald J. Trump was sworn in as the 45th President of the United States of America.]

The Department of Housing and Urban Development announced on Monday that they plan to reduce the Mortgage Insurance Premium for FHA mortgage loans. Since 2012, the Federal Housing Administration’s(FHA) Mutual Mortgage Insurance(MMI) Fund has gained $44 billion, and is now 32 basis points above the 2 percent threshold level required by Congress. This is ~$13 billion more than projected for Fiscal Year 2017 in an Actuarial Review of the MMI Fund for Fiscal Year 2012.

“After four straight years of growth and with sufficient reserves on hand to meet future claims, it’s time for FHA to pass along some modest savings to working families,” … “This is a fiscally responsible measure to price our mortgage insurance in a way that protects our insurance fund while preserving the dream of homeownership for credit-qualified borrowers.” – Julián Castro, HUD Secretary

According to the FHA, the reduction will return the Mortgage Insurance Premium nearly to levels seen before the housing bubble crisis. The FHA also predicts that ~1 million borrowers will buy or refinance with an FHA loan over the next year, most of whom will see reduced costs.

“We’ve carefully weighed the risks associated with lower premiums with our historic mission to provide safe and sustainable mortgage financing to responsible homebuyers,” … “Homeownership is the way most middle class Americans build wealth and achieve financial security for themselves and their families. This conservative reduction in our premium rates is an appropriate measure to support them on their path to the American dream.”

– Ed Golding, Principal Deputy Assistant Secretary for HUD’s Office of Housing.

According to the FHA, annual mortgage insurance premiums will be lowered 25 basis points*, or one quarter of one percent, will come into effect on January 27th of this year. The FHA estimates that new rates could save, on average, $500 in 2017 alone for most FHA borrowers.

*For loans less than or equal to $625,500 with a maturity greater than 15 years. Please see the full report from HUD for more details of different loan scenarios and their actual MIP’s.

Call or contact me today! Get started today. Find Your Branch here: Get Started Now!

The Federal Housing Finance Agency has announced that it is increasing the maximum conforming loan limits for mortgage loans beginning in 2017. A mortgage loan is considered “conforming” when it is eligible to be acquired by Fannie Mae and/or Freddie Mac. (Mortgages are often sold to Fannie or Freddie so that a lender has the liquidity/money available to issue more mortgage loans for home buyers.)

The current 2016 loan limit for single-unit properties or single family homes has remained at $417,000 for the last 10 years until recently. The FHFA has announced that the loan limit for single-family homes is increasing approximately 1.7% on January 1, 2017 from $417,000 to $424,100.

The changes were established because of The Housing and Economic Recovery Act of 2008 [pdf], which previously set the baseline loan limit at $417,000. The law also determined that after a period of housing pricing declines, the loan limit may not rise until prices return to pre-decline levels. It follows that since the FHFA is increasing the limit, it stands to reason that home pricing is back to pre-decline levels!

See also: Low Housing Inventory Driving Values Up – Benchmark (why the latest rise in home pricing is not another bubble)

The FHA national loan limit “ceiling” will rise to $636,150, formerly set at $625,500. Additionally, the “floor” will increase to $275,665 from $271,050. The actual limit is variable by state and county. The “floor” is the lowest assigned limit, and the “ceiling” is the highest assigned limit for the nation as a whole.

The national loan limit is recalculated annually by the FHA from a percentage calculation of the national conforming loan limit. The calculated increase is positively correlated with rising home prices in high-cost markets.

It means that the Department of Housing and Urban Development has taken notice of the trend of rising home prices. It also means that borrowers will be able to borrow more than they previously could without affecting the ability of lenders to maintain liquidity.

It’s a great time to buy!