A VA Home Loan, you may be aware, offers up to 100% financing for eligible veterans and military service members. This means that the Department of Veteran Affairs VA Loan program allows qualified borrowers the ability to purchase a home with no down p...

2018 Homeownership Profiles: Millennial Buyers

In 2017, Australian millionaire Tim Gurner famously attempted to blame millennial homebuyer obstacles on their inability to avoid frivolous spending on $19 avocado toast, in comments that were widely mocked throughout the internet.

Many commentators are still quick to point the finger at extravagant spending to explain why homeownership among younger adults has declined compared to previous generations. However, the more likely culprit is soaring student loan debt and a limited supply of homes causing rapidly inflating prices, which is making it more difficult for millennials to afford homes.

Despite what you hear, it’s not all doom and gloom for aspiring millennial homebuyers. According to the National Association of Realtors (NAR) latest study, millennials continue to be the largest generational cohort of buyers, making up 36% of the purchase market.

Check out the latest statistics and trends among this influential bloc of homebuyers.

Stats About Millennials

Many people still think of millennials as teenagers, instead of young adults in their 20’s and 30’s who currently make up the largest generation in the workforce. NAR’s study defines millennials as buyers age 20-37.

Of this group:

- 22% of millennial buyers are age 20-27, while 78% are age 28-37. The median age was 31.

- 66% were married couples, 18% were single, and 15% were unmarried couples

- 65% were first time homebuyers

- Prior to buying, 56% rented an apartment or house, 18% lived with parents/relatives/or friends, and 24% owned a previous home

Millennials As Homeowners

- 89% purchased previously built homes and 11% purchased new homes. Better price was cited as the number one reason buyers purchased previously owned homes.

- Quality of the neighborhood, convenience to job, and overall affordability of homes were the top reasons millennial buyers chose their neighborhood.

- The median purchase price was $220,000

- 44% paid asking price or higher for their home

Millennials and Home Financing

- 98% of millennials financed their home purchase, compared to 88% overall

- 75% used savings for the down payment, 23% used gift funds, and 21% used proceeds from the sale of a primary residence (respondents could select more than one source)

- 53% reported that student loans delayed saving for a home

- 55% reported that they made sacrifices to non-essential items like entertainment and vacations to save for a home

- 67% found the mortgage application and approval process not difficult or easier than expected.

- Only 6% of millennial buyers had a previous mortgage application denied. The number one reason was for debt-to-income ratio, followed by low credit score.

- 46% of buyers had student loan debt. The median amount was $27,000.

- 55% used a conventional loan, 27% used an FHA loan, and 10% used a VA loan.

After analyzing their demographics and buying habits, it is clear that millennial buyers have become a powerful force in the housing market. As it turns out, avocado toast is not preventing millennials from buying homes.

How To Avoid Roadblocks Before Closing On Your New Home

You have submitted a mortgage application, found your dream home, and put in an offer. Now what? Applying for a home loan is an ongoing process, from application to closing, that does not have to be stressful. There are several things you can do to make the process more efficient, and things not to do to avoid delaying your closing or changing the status of your approval. Below is a list of recommendations to make sure that this exciting journey progresses as smoothly as possible, all the way up to the day you receive your keys.

DO:

Pay bills on time

Remember to stay current on your existing accounts. Set reminders for yourself or place bills on autopay to avoid late payments, as they could cause a delay in your closing.

Postpone career moves until after closing

Your approval is based on your current employment and income, and both need to be verified. Making career changes, regardless of the compensation, will make the verifications obsolete and cause the loan file to repeat the underwriting step. Of course, there are instances where you may not be able to control these changes. If you are considering a job change or experience an unexpected job change, give us a call.

Keep financial documents available

We try to collect everything up front, however, our Underwriting team may request additional documentation. We recommend that you keep your financial records easily accessible until after closing.

Save your income statements

Keep all current and upcoming income statements. There will be additional verbal verifications with your employer and your CPA, and verification of your IRS tax transcripts. Everything will need to match, so hang onto your incoming paystubs, as they may need to be updated by your underwriter.

Save all pages of your bank statements

These pages may need to be updated, so be sure to keep upcoming bank statements available. This applies to all checking and savings accounts, along with any brokerage and retirement accounts.

DO NOT:

Make any large purchases (such as a boat or car)

Similar to the way a new credit card or credit inquiry can prevent us from being able to close your loan, making a large purchase before your closing can delay your move-in date. If you must make a large purchase, give us a call first to determine what kind of impact it could have.

Make any unusually large deposits

Money used for a down payment on your home may not be borrowed money, and you will need proof that large deposits are not borrowed funds. A large deposit is defined as any amount greater than 25% of any one borrower’s monthly net income deposit.

Close credit card accounts

Closing a credit card will reduce your total amount of available credit, impacting your credit score. New credit can bring your credit score down as well, so it’s best to postpone opening any new credit accounts until after closing. (see the next Do Not)

Apply for new credit

New credit inquiries can have a negative impact on your credit score and your debt-to-income ratio. Any changes can create delays, change the terms of your loan, or cause your loan to be denied, in some cases. If you must open a new account, consult with us first, and we will analyze and properly document the impact.

Be afraid to ask questions

If you are uncertain about what you need to do, or which steps you should take, we at Benchmark are here to help you through the process. Together, we can work towards a truly great experience purchasing your brand new home!

Construction Loans: What to Expect

Building a new home offers many advantages over purchasing an existing home on the market. You are able to customize the home to your specific needs and preferences and avoid costly repairs of outdated features. New homes are often also more energy efficient and technologically equipped.

Different from Traditional mortgages.

Securing financing for a construction loan does differ from obtaining a traditional mortgage, however. Since the home is not yet built, there is more risk for the lender because the home being purchased is used as collateral for the loan. In other words, there is no present collateral to back the loan before it is approved. Much like applying for a traditional mortgage, you will be required to submit documentation pertaining to your income, assets, and credit history to determine if you meet requirements set by the lender to qualify for the construction loan. You and your builder will also provide detailed documentation on the building plans and construction timeline to the lender to evaluate the ability for the project to be completed on time and within budget.

Because of the increased risk that comes with building a house, you can typically expect to need a credit score of 700+ with a sizeable down payment of at least 10-20%. The specific requirements will vary based on your lender and the type of construction loan you choose.

One-Time-Close, or “Construction-to-Permanent” loans

A one-time-close construction loan, also commonly known as a construction-to-permanent loan, is a popular choice among borrowers, because it allows you to avoid the extra expense of two closings when building your new home. Because construction and permanent financing are combined into one loan, you will save on costs associated with title and appraisal fees that would occur if there were two separate closings.

With a one-time close program, the borrower will take out all of the financing to build the home, and the loan is closed before starting construction. Permanent house payments will not typically begin until the construction is completed. The loan is funded as the house is being built through construction draws to the builder. In order to receive these draws, the lender will conduct regular check-ins and inspections of the property to ensure the project is being completed according to the plans and timeline. Generally, you are making interest-only payments as the builder draws funds to build the home. Once construction is completed, the loan will be converted into a permanent note, and your permanent monthly house payment will begin.

In Summary…

Construction loans are a great option for aspiring home owners who want to build their custom dream home from the ground up. While the process differs from obtaining a mortgage on an existing home, your lender can walk you through the process and advise you on the advantages and disadvantages of undergoing a building project.

Have questions about construction financing? Get in touch with me or call me !Get in touch with your local Benchmark branch!Get in touch with us!

Benchmark Introduces New Program to Expand Options for Medical Professionals

Benchmark has launched a new mortgage product that is customized to the unique career and financial outlook of professionals in the medical field. Last year, we launched the Medical Doctor Loan Program to better serve medical residents and doctors. Now we have further expanded our options for medical professionals to include jumbo loan amounts up to $2 Million with our Preferred Medical Professional Program.

The new Preferred Medical Professional Program is tailored to meet the needs of medical doctors within 10 years of residency, dentists and veterinarians OR newly licensed medical residents/students who are currently employed or starting new employment within 60 days of closing.

At Benchmark, we understand what it has taken to get to this point in your medical career, so we designed our new Preferred Medical Professional Program to maximize your money, and even to exclude student loan debt in certain cases:

- Loan Amounts up to $2 million1

- Student loan debt that is deferred for at least 12 months may be excluded from Debt-to-Income (DTI) calculations

- Purchase and limited cash-out refinances

- Loan-to-Value (LTV) up to 95%2

- Available on 5/1, 7/1, 10/1 + 15/1 Adjustable Rate Mortgages (ARMS)

1 minimum loan of $453,101 in most areas

2 LTVs ≥ 90% requires Lender Paid Mortgage Insurance

Want to learn more about your home financing options available through Benchmark? Get in touch with me.Find your branch to get started.Select your loan officer to get started.

Ark-La-Tex Financial Services, LLC 5160 Tennyson Pkwy STE 1000, Plano, TX 75024. NMLS ID #2143 (www.nmlsconsumeraccess.org) 972-398-7676. This advertisement is for general information purposes only. Some products may not be available in all licensed locations. Information, rates, and pricing are subject to change without prior notice at the sole discretion of Ark-La-Tex Financial Services, LLC. All loan programs subject to borrowers meeting appropriate underwriting conditions. This is not a commitment to lend. Other restrictions may apply. (https://benchmark.us)

How to Buy in a Competitive Summer Market

The weather is heating up, and so is the summer housing market.

With more buyers entering the market looking to find a new home during the summer months, competition can be fierce. Every homebuyer’s nightmare is finding their dream home, only to lose it in a multiple-offer scenario that drives the asking price up beyond your reach. How can you make your offer stand out in an aggressive housing market? Here are a few ways to get an edge.

Use an Experienced Agent

Think of your real estate agent as the MVP of your home buying team. The right agent will not only make your home search easier, but they can also help improve your chances when making an offer. An experienced agent will work with you to craft a great offer, and will be responsive and professional in discussions will the seller. Having a professional on your team who is knowledgeable about the local market could be the difference between your offer being accepted or rejected.

Get Pre-APPROVED

A lot of homebuyers assume that pre-qualification and pre-approval for a mortgage are the same thing. In fact, they are quite different, and which one you get can make a huge difference in the eyes of the seller. A pre-qualification is only an estimate of what you qualify for based on the income, assets, and debt information you provide. It does not include an analysis of your credit report or verification of the financial information you provide. On the other hand, getting pre-approved means your loan officer documents and verifies your financial information and reviews your credit report. After evaluation, they can issue a specific loan amount you are approved for.

A seller in a multiple-offer scenario will immediately see through a pre-qualification, and worry that if they accept your offer, the deal might fall through if you are unable to secure your home financing. A pre-approval makes your offer stronger and puts you in an optimal negotiating position.

Set Realistic Expectations

Setting realistic expectations can help reduce your stress during the home buying process. Making an offer on a home can be nerve-wracking, so it is a good idea to go into negotiations already knowing your bottom line. Make a list of what you are willing to compromise on – whether it’s sale price, contingencies, or closing costs – before you make your initial offer. Don’t let a high-stress multiple-offer situation make you commit to something that does not make financial sense for you and your family. It can be disheartening if your offer is not accepted. If this happens, just keep your head up, and continue your home search armed with your pre-approval from your lender, and the expertise of your real estate agent.

Ready to look for your new home this summer? Contact me, call , or apply now to get pre-approved.Find your local loan officer to get pre-approved.Meet the team, Contact us, or Select your loan officer to get pre-approved.

Boot’n & Shoot’n 2018 Raises $1Million for Veterans

DALLAS, TX—The month of April means the first full month of Spring, wildflowers, and the arrival of what former Governor Rick Perry described as “the most patriotic day in Texas:” Boot’n & Shoot’n.

Boot’n & Shoot’n is an annual event to raise money for US military veterans who risked it all. For the second year in a row, Boot’n & Shoot’n has reached 1 million dollars in funds raised to help deserving veterans and their families.

Hosted at the Dallas Gun Club, 90 teams of clay shooters each teamed up with a veteran for a day of sporting clays, a live concert, country style food sponsored by Babe’s Chicken, and a live auction. 100% of all proceeds is given to organizations which exist solely to aid veterans and their families, including The Brain Treatment Foundation, 22Kill, and Third Option Foundation. Founded in 2012 as the vision of Benchmark Founding Partner Stewart Hunter and his wife Janet Hunter, this year marks the 7th annual event. To learn more, visit BootShoot.com.

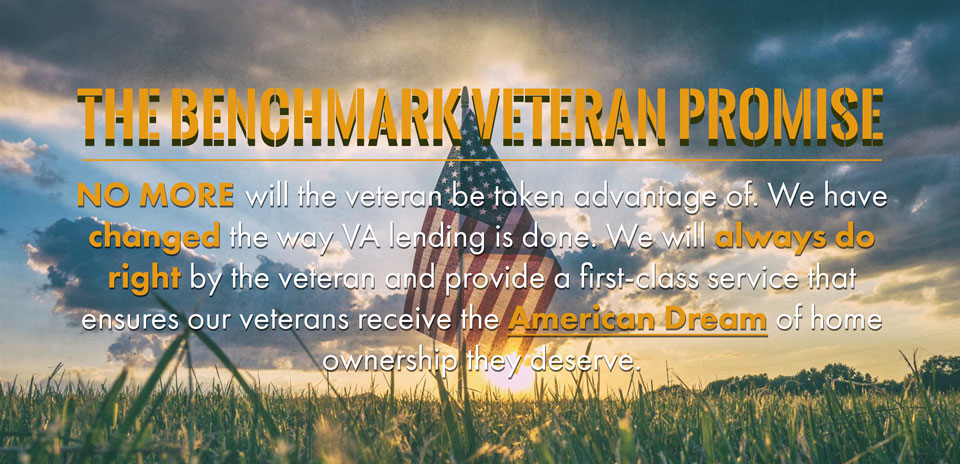

Announcing “The Veterans Homefront by Benchmark”

NO MORE

These are the words that Benchmark has adopted when it comes to Veteran lending. Benchmark is proud to kick off The Veterans Home Front initiative which aims to do right by our Military men and women. The veteran lending space has long been a marketplace in which Veterans have been taken advantage of, have not been given proper service, or have been subject to predatory lending. Benchmark believes that our heroes who choose to serve this nation deserve the outstanding service that Benchmark has been providing since 1991. We are dedicated to doing right by the veteran, and have created an educational course that will certify our Loan Officers to be VA Certified. This certification will ensure that we not only get the veteran in the best loan product for them, but also are able to assist our veterans with maximizing their VA benefits.

![]()

Visit The Veterans Homefront

https://theveteranshomefront.com

Benchmark is the proud founder and title sponsor of Boot’n & Shoot’n (bootshoot.com), a veteran giveback event that has been called “The most patriotic day in Texas” by former Texas Gov. Rick Perry. To date, Boot’n & Shoot’n has raised over $4 Million and has been able to provide over 30 scholarships to veterans so they can receive state of the art treatment for traumatic brain injury and post-traumatic stress from The Brain Treatment Foundation. We are excited to kick off this initiative that will allow Benchmark to welcome our veteran heroes home.

Learn more about Boot’n & Shoot’n at bootshoot.com.

Homeownership and Your 2017 Tax Return

The deadline to file your 2017 tax returns is approaching on April 17th. If you have not filed your taxes yet, you can take this opportunity to talk to your tax professional about how homeownership may impact your tax return this year. Here are a few reasons why you may want to.

Mortgage Interest may be tax deductible

According to the IRS, taxpayers may deduct interest on up to $1,000,000 of their qualified home loan on 2017 tax returns. If you are married filing separately, you can deduct up to $500,000.

Under the Tax Cuts and Jobs Act of 2017, for home purchases after December 15th, 2017, interest may only be deducted on qualifying mortgage debt up to $750,000 when filing 2018 tax returns.

Property Taxes may be tax deductible

Homeowners who itemize deductions on their tax return may be able to deduct property taxes on their primary residence, as well as other real estate they own. Take advantage of this deduction now, because when you file your 2018 tax return next tax season, under the Tax Cuts and Jobs Act of 2017, homeowners will be limited to deducting up to $10,000 in personal state and local property taxes.

Talk to your tax professional

Your trusted tax professional can help you determine how homeownership impacts you as a taxpayer. Be sure to ask about state exemptions, as they vary. The good news is that most changes to the tax code will not affect 2017 taxes if filed before the April 17th deadline. Although several changes that affect homeowners will go into effect next tax season in 2018. While the new law will lower the caps for itemized deductions, the standard deduction will nearly double. So unless you have enough itemized deductions to exceed the increased standard deduction, many of the changes discussed will not affect your return.

Ark-La-Tex Financial Services, LLC NMLS ID #2143 (www.nmlsconsumeraccess.org) is not a law firm, accounting firm, tax firm, or financial planning firm. This advertisement is for general information purposes only. Anyone relying on particular details contained herein does so at his or her own risk and should independently use and verify their applicability to a given situation. (https://benchmark.us)

Pre-Qualification vs. Pre-Approval: What’s the difference?

Looking at homes without knowing how much you can afford can be a waste of time for you and your realtor.

“Give me six hours to chop down a tree and I will spend the first four sharpening the axe.”

unknown

The same wise sentiment can apply to purchasing a home – why start house hunting without putting in the time to get pre-approved so you can know your budget?

Armed with misconceptions, many home buyers mistakenly think that pre-qualification and pre-approval for a mortgage are the same thing. In reality, there is a big difference between these two terms. Understanding the distinction could be the difference between having your offer on a house accepted or rejected.

PRE-QUALIFICATION

During a pre-qualification, you provide your lender with your overall financial picture (including your income, asset, and debt information). After evaluating this information, your loan officer can give you a good estimate of what you qualify for. A pre-qualification does not include verifying the information you provide, nor an analysis of your credit report. Because of this, a pre-qualified buyer does not carry the same weight as a pre-approved buyer when making an offer on home.

PRE-APPROVAL

Pre-Approval is when you complete an official loan application and provide your loan officer with the necessary information to document and verify your income, assets, and debts. Your lender will pull your credit report and look over documents such as bank statements and W-2s. From this analysis, the loan officer can tell you the specific amount for which you are approved, and which loan programs might be the best fit for your unique financial situation.

| Pre-Qualification | Pre-Approval | |

| Based on Estimates | ||

| Based on documented information | ||

| Income, Assets, and Verified Credit | ||

| Written conditional commitment | ||

| Shows serious intentions to buy | ||

| Gives strongest negotiating power |

Bottom Line?

A pre-approval carries a stronger weight with sellers and puts you in the best negotiating position possible.

Want to get pre-approved before looking at homes? Start by Contacting Me, or Apply Now.

Want to get pre-approved before looking at homes? Find you loan officer to get started, or Apply Now.

Want to get pre-approved before looking at homes? Drop us a line, or Apply Now with our branch manager or your loan originator.