Should you buy a home in the spring, or should you wait? Here are four good reasons to buy now.

Should you buy a home in the spring, or should you wait? Here are four good reasons to buy now.

Most agree that home prices have risen, and are still on the rise. We have written about why this is not like the housing bubble that we saw nearly ten years ago. In some areas, there are not enough homes for sale to meet the demands of home buyers, and prices are driven up organically. see – Low Housing Inventory Driving Values Up – Benchmark

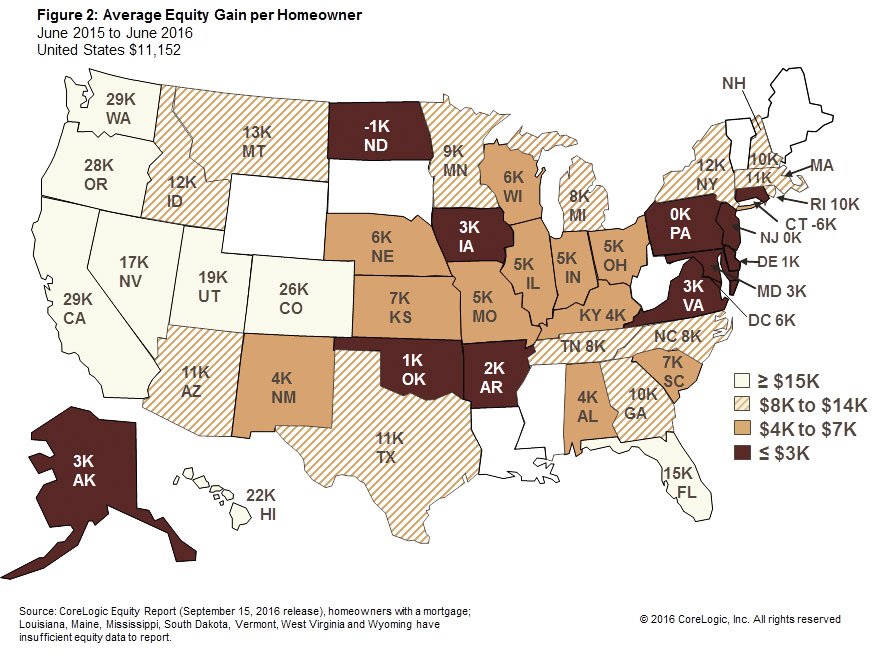

While this can make things more difficult for some home buyers, there is a bright side. The average household in the US gained over $11,000 in equity in the last year owing, at least in part, to rising home values, according to CoreLogic’s most recent US Economic Outlook.

This map is originally provided by CoreLogic’s report. This shows the average, by state, of home equity gained per homeowner from June 2015 to June 2016. The national average equity gain per homeowner was $11,152.

To address any fears that this nationwide appreciation harkens back to the bubble burst a decade ago, please recognize that homeowners are investing this new equity in their homes and in themselves rather than in speculation or assets subject to standard depreciation.

What does this mean? This means that it is probably helping families to pay for college, start small businesses, pay off their mortgage faster, or moving to a home more suited to their dreams or lifestyle.

CoreLogic’s predictions are that home prices will rise another 5% by this date in 2017. Would you believe that it is still cheaper to buy than to rent? Stay tuned for our next post!

Many people may have been watching home values steadily rise over the past year, and notice that it isn’t slowing down.

Is this the aftershocks of 2008? Has sub-prime lending made a comeback as the Federal Reserve has hesitated to raise interest rates? Are new homeowners soon to be upside down on their young mortgages? No. Some have speculated it. Don’t believe it.

After the bubble crash 8 years go, demand dropped first, then supply followed. In the market’s rebound correction (that we are still in the middle of), demand is driving the housing market once again.

In this case, demand growth is outpacing the housing supply. The result? More people want the housing that is available, and the competition drives up market value.

While this does make it a difficult time to buy, it may also be a terrific time to sell!

When prices are going up, and are projected to continue to increase, it is good to remember that interest levels are still low. This is when it makes sense to consider the true cost of waiting.

Consider this:

If you were to buy a house right now, with a $250,000 mortgage at 3.68%APR interest, your Payment (P&I) would be $1,147.88

If you were to buy the same house Between January and March (estimate) in 2017, your same mortgage would be $263,750 at (estimated) 4.5%APR interest. Your Payment (P&I) would be $1,336.38

By buying now, your net worth would automatically increase by $13,750 (not including the principle payments that you would be making to shrink the balance/increase your equity)

The difference in monthly payment would be $188.50. Can you afford an extra $188/month in exchange for… uh… well… …hesitation?

Over the course of 30 years, you would end up paying $67,860 more as a result. What could you do with an extra $68k?

The general convention, as we have mentioned before, is to buy as early as you can. You may be better off in terms of both equity and housing costs.

Ready to get started? Give us a call!

Your home’s mortgage payment is based on the price of the home (minus the down payment), and the interest rate for the loan.

Both prices and interest rates will likely rise in 2016.

CoreLogic anticipates a national 5.2% home value increase for the next year. The percentage varies by state, with WA, CA, NV, UT, AZ, NM, FL, and VT seeing the greatest increase at an average of 7.6% (the highest being CA at 10.8%, the lowest of this group being NM at 6.0%). The lowest forecasted home price increase is WV at 1.3%. Clearly, the majority of the country is projected to see a real home value appreciation that outpaces currency inflation (0.5% from 2014-2015).

Which reminds one of this post: click here

All four establishments who provide future projections on mortgage interest rates agree that rates will rise in 2016. The following table shows the change for each quarter of the next year.

| Quarter | Fannie Mae |

Freddie Mac |

MBA | NAR | Average of all four |

| 2016 1Q | 3.9 | 4.0 | 4.2 | 4.1 | 4.05 |

| 2016 2Q | 4.0 | 4.2 | 4.4 | 4.3 | 4.23 |

| 2016 3Q | 4.0 | 4.4 | 4.6 | 4.6 | 4.4 |

| 2016 4Q | 4.1 | 4.6 | 4.8 | 4.9 | 4.6 |

Since home prices and interest rates expected to increase over the next year, it makes sense to buy sooner rather than later, if you are buying a new home.

Higher home prices are expected by 33% of consumers over the next year.

Fannie Mae’s monthly housing survey indicated 5% more people expect home prices to increase this month over the 27 percent surveyed last month who thought prices would increase this year.

Nearly half of consumers expect higher rental prices as well, the highest number registered by Fannie Mae since its monthly tracking began in June 2010. Americans’ rental price expectations for the next year continue to rise, reaching their record high level for the Fannie Mae survey this month.

The percentage of respondents who say it is a good time to buy rose by three points to 73 percent, the highest level in more than a year, while the percentage of respondents who say it is a good time to sell rose one point to 14 percent this month.

Consumers’ confidence about their own finances is stabilizing, with 44 percent expecting an improvement over the next year.

Higher Mortgage Rates Expected

There is an increasing share of consumers expecting both higher mortgage rates and home prices over the next 12 months.

Doug Duncan, Vice President and chief economist of Fannie Mae says, “Americans’ rental price expectations for the next year continue to rise, reaching their record high level for our survey this month.”

Duncan says, “Some may feel that renting is becoming more costly and that home ownership is a more compelling housing choice. Conditions are coming together to encourage people to want to buy homes.”

While the “sales of existing homes in January and February marked the strongest start to a year since 2007,” according to the combined Housing and Urban Development (HUD)/Treasury statement. “Data on home prices changed little from the previous month – marking a fifth month of seasonal lows.”

For further Fannie Mae survey findings, visit the Fannie Mae Monthly National Housing site.

Here’s an interesting chart from the U.S. Census Bureau website about the average price of a home in the U.S.

Take a look at how fast homes shot up from 2000 – 2007: over $100,000!

Period Average

1963 $19,300

1964 $20,500

1965 $21,500

1966 $23,300

1967 $24,600

1968 $26,600

1969 $27,900

1970 $26,600

1971 $28,300

1972 $30,500

1973 $35,500

1974 $38,900

1975 $42,600

1976 $48,000

1977 $54,200

1978 $62,500

1979 $71,800

1980 $76,400

1981 $83,000

1982 $83,900

1983 $89,800

1984 $97,600

1985 $100,800

1986 $111,900

1987 $127,200

1988 $138,300

1989 $148,800

1990 $149,800

1991 $147,200

1992 $144,100

1993 $147,700

1994 $154,500

1995 $158,700

1996 $166,400

1997 $176,200

1998 $181,900

1999 $195,600

2000 $207,000

2001 $213,200

2002 $228,700

2003 $246,300

2004 $274,500

2005 $297,000

2006 $305,900

2007 $313,600

2008 $292,600

2009 $270,900

2010 $272,900

Data through April 2011, released yesterday by S&P/Case-Shiller Home Price Indices, the leading measure of U.S. home prices, show a monthly increase in prices for the 10- and 20-City Composites for the first time in eight months. The 10- and 20-City Composites were up 0.8% and 0.7%, respectively, in April versus March.

In April 2011, the 10-City and 20-City Composites recorded annual returns of -3.1% and -4.0%, respectively. On a month-over-month basis, the 10- and 20-City Composites were up 0.8% and 0.7% in April versus March.

“In a welcome shift from recent months, this month is better than last – April’s numbers beat March,” saysDavid M. Blitzer, Chairman of the Index Committee at S&P Indices. “However, the seasonally adjusted numbers show that much of the improvement reflects the beginning of the Spring-Summer home buying season. It is much too early to tell if this is a turning point or simply due to some warmer weather.

As of April 2011, average home prices across the United States are back to the levels where they were in the summer of 2003. Measured from their peaks in June/July 2006 through April 2011, the peak-to-current declines for the 10-City Composite and 20-City Composite are -32.6% and -32.8%, respectively. From their April 2009 troughs, the 10-City Composite has risen 1.4% and the 20-City Composite is up a scant 0.7%.

The table below summarizes the results for April 2011. The S&P/Case-Shiller Home Price Indices are revised for the 24 prior months, based on the receipt of additional source data. More than 24 years of history for these data series is available, and can be accessed in full by going to www.homeprice.standardandpoors.com

| April 2011 | April/March | March/ February | ||

| Metropolitan Area | Level | Change (%) | Change (%) | 1-Year Change (%) |

| Atlanta | 101.95 | 1.6% | -0.3% | -3.5% |

| Boston | 147.07 | -0.2% | -1.7% | -4.2% |

| Charlotte | 108.42 | -0.3% | -1.2% | -6.6% |

| Chicago | 110.12 | -0.4% | -2.4% | -8.6% |

| Cleveland | 97.69 | 1.2% | -1.8% | -6.8% |

| Dallas | 113.38 | 0.5% | -0.8% | -4.0% |

| Denver | 122.32 | 1.5% | -0.6% | -4.1% |

| Detroit | 62.74 | -2.9% | -4.4% | -7.5% |

| Las Vegas | 96.47 | -0.7% | -1.1% | -6.2% |

| Los Angeles | 168.20 | 0.3% | -0.3% | -2.1% |

| Miami | 136.99 | -0.2% | -0.8% | -5.6% |

| Minneapolis | 106.07 | 0.4% | -3.7% | -11.1% |

| New York | 164.17 | 0.8% | -1.0% | -2.8% |

| Phoenix | 100.36 | 0.1% | -0.5% | -8.8% |

| Portland | 132.84 | 0.1% | -0.7% | -9.2% |

| San Diego | 154.50 | 0.4% | -0.8% | -4.3% |

| San Francisco | 132.03 | 1.7% | -0.1% | -5.5% |

| Seattle | 135.14 | 1.6% | 0.1% | -6.9% |

| Tampa | 126.47 | -0.4% | -0.5% | -7.7% |

| Washington | 186.76 | 3.0% | 0.2% | 4.0% |

| Composite-10 | 152.51 | 0.8% | -0.8% | -3.1% |

| Composite-20 | 138.84 | 0.7% | -0.9% | -4.0% |

| Source: Standard & Poor’s and Fiserv | ||||

| Data through April 2011 | ||||

Read the full report at HousingViews.com.