In this episode of ‘On the House,’ we uncover the diverse world of mortgage products beyond the 30-year fixed rate. From Fannie Mae to FHA and VA loans, discover options for first-time buyers, low credit borrowers, and more. Learn about down payment assistance and why working with a loan officer is key to finding the perfect fit.

Video:

Host: Jason Haeger – Host | On The House Podcast

Guest: Mary Ann Pallitto – Product Development Specialist

Want to see if homeownership is right for you? Reach out to your local Benchmark branch to learn more. https://benchmark.us/

Legal Disclaimer:

The information provided in this presentation is for general informational purposes only. The content shared here is not intended to be financial, legal, or professional advice specific to your situation. Mortgage regulations and requirements may vary, and the information discussed may not be applicable to your individual circumstances. Therefore, we recommend consulting with a qualified professional or contacting Ark-La-Tex Financial Services, LLC – NMLS #2143 directly for personalized advice tailored to your needs. Any reliance you place on information from this presentation is at your own risk. By listening to this presentation, you acknowledge and agree that Ark-La-Tex Financial Services, LLC – NMLS #2143, its hosts, and guests are not responsible for any losses, damages, or liabilities that may arise from your reliance information presented here. Ark-La-Tex Financial Services, LLC NMLS# 2143 (www.nmlsconsumeraccess.org). All loans subject to borrower qualifying. This is not a commitment to lend. Other restrictions may apply. (https://benchmark.us)

The insurance industry has experienced significant changes over recent years, with homeowner’s and auto insurance rates increasing rapidly. The reasons behind these trends are numerous, involving a combination of economic, environmental, and market-driven factors.

Homeowner’s insurance on the rise

Homeowner’s insurance rates have risen notably, driven by several unrelated critical factors:

Rising Rebuilding and Replacement Costs: Between 2019 and 2022, the costs associated with rebuilding and replacing homes climbed by 55%1. This increase is a principal driver behind higher premiums as insurers recalibrate to cover these escalated costs.

Extreme Weather Impacts: A rise in natural disasters, including severe storms and wildfires, has heavily impacted the insurance sector2. The increase in these catastrophic events have lead to more large claims, driving up costs for insurers. Costs which, in turn, get passed on to homeowners.

Market Pressures and Area Exits: Worsening financial performance has caused property insurance market to experience significant strains, which are partly due to economic inflation and changes in exposures3. These pressures have resulted higher premiums and, in some cases, insurers exiting certain markets (no longer writing polices in certain regions) or reducing their policy offerings4.

Accelerating auto insurance premiums

Auto insurance has also experienced rate increases, with overlapping and unique factors to blame:

Rising Inflation and Repair Costs: Similar to homeowners insurance, auto insurance is impacted by inflation. The cost of repairs, labor, and parts has increased, leading insurers to raise premiums to cover these higher expenses5.

More Natural Disasters: Auto insurance companies were also impacted by natural disasters, which can lead to a higher volume of claims. Vehicles damaged by storms, floods, or fires contribute to the overall risk insurers need to manage5.

More Technological Complexity: Modern vehicles come equipped with advanced technology, making repairs more expensive. This novel complexity adds to the overall cost insurers need to cover, contributing to premium increases.

Common themes and relationships in insurance

Analyzing the causes behind the steep rise in both homeowners and auto insurance rates reveals common themes:

Impact of Weather Extremes: Both sectors are significantly affected by climate change, leading to an increase in natural disaster-related claims. This trend underscores the growing importance of environmental factors in insurance pricing.

Economic Factors: Inflation plays a crucial role in both contexts, impacting the cost of repairs, replacements, and labor. Economic conditions directly influence insurance rates, reflecting broader market dynamics.

Technological and Material Costs: Just as the cost of modern vehicle technology impacts auto insurance, the rising costs of building materials and construction technology affect homeowners insurance. These factors contribute to the overall increase in premiums.

Looking ahead

Understanding these trends is critical for consumers looking to navigate the changing insurance landscape effectively. While external factors like climate change and inflation may be beyond individual control, there are steps consumers can take to mitigate the impact on their insurance rates. Regularly reviewing policies, improving property resilience, and shopping various insurance providers can help secure more favorable terms.

Given the complex interplay of factors driving insurance rates up, it’s evident that both homeowners and auto insurance sectors are navigating through a period of adjustment. Awareness and proactive management of insurance policies become even more crucial to adapt to these changes.

What’s a future homeowner to do?

It’s no secret that inflation has taken a bite out of the average worker’s spending power. The general cost of living is, on average, higher than it used to be. See the chart below of the latest 5-year trend of the Consumer Price Index in the United States using data from the US Bureau of Labor Statistics:

If you currently rent your home, you may also have noticed that the average cost to rent has risen as well. Below is a chart of Rent Inflation for the past 5 years, again, using data from the US Bureau of Labor Statistics:

If you are feeling the pinch of inflation and rent increases, you may be tempted to believe that the American Dream of homeownership is slipping away. Headlines have emphasized the increase in mortgage rates, and it’s no secret that demand has buttressed home prices, as indicated in the chart below using data from the Federal Housing Finance Agency (FHFA):

United States FHFA House Price Index: Last 5 Years

What if you could do something now to help prepare for a more expensive future? What if homeownership is more than just a foundational part of the American Dream, but a tool to leverage a better financial future for family, or just for yourself?

Fight rent increases: Fire your landlord. (and become your own)

Maybe you love your landlord. Maybe you really dislike your landlord. Either way, the odds are good that your rent is higher than it was 2 years ago (Remember the rent inflation chart above?).

You know what isn’t higher? The principle and interest monthly payment for a mortgage that started 2 years ago. That’s the magic of a mortgage loan: the monthly payment doesn’t change for the life of the loan. Sure, this doesn’t account for insurance rates, taxes, or HOA fees, but every dollar you pay on the principle is equity in your home that you now own, and your lender doesn’t. You can’t say that about rent.

Your home as a financial asset

As the property you own increases in value, you own every bit of the new value, and your monthly payment (principle and interest) stays the same. Maybe you have a growing family, or you want a bigger garage, office, space to entertain, or whatever you have your heart set on. If you want to get a bigger house, you can take the equity of your existing house, and use it to help pay for your next house.

Over time, as your equity grows (and your monthly principle and interest payment stays the same), your net worth and economic resilience grows with it. In fact, if you want an even lower monthly payment, you may be eligible to refinance your remaining debt into a new mortgage, if rates are favorable. You could also use a portion of the equity in your home for other expenses. (These are referring to various loan products, and the best product for your situation may not be the same the best option for someone else.) The point is, becoming a homeowner gives you options that are not available otherwise.

Know your options

If you firmly believe that homeownership is out of reach, we encourage you to explore your options anyway. There are a variety of programs, and a variety of properties that can work together to help you start building home equity. If qualification is a problem, there are steps you can take to work towards qualification.

The point is, don’t let your own limiting beliefs hold you back. Our team of loan experts thrive on helping buyers overcome challenges to help you fire your landlord, become a homeowner, fight back against rising rents, and start building equity.

If you are ready to get started, fill out our no-obligation form, and your mortgage loan expert will contact you to help you determine your best path forward.

The information provided in this presentation is for general informational purposes only. The content shared here is not intended to be financial, legal, or professional advice specific to your situation. Mortgage regulations and requirements may vary, and the information discussed may not be applicable to your individual circumstances. Therefore, we recommend consulting with a qualified professional or contacting Ark-La-Tex Financial Services, LLC – NMLS #2143 directly for personalized advice tailored to your needs. Any reliance you place on information from this presentation is at your own risk.

By listening to this presentation, you acknowledge and agree that Ark-La-Tex Financial Services, LLC – NMLS #2143, its hosts, and guests are not responsible for any losses, damages, or liabilities that may arise from your reliance information presented here.

Ark-La-Tex Financial Services, LLC NMLS# 2143 (www.nmlsconsumeraccess.org). All loans subject to borrower qualifying. This is not a commitment to lend. Other restrictions may apply. (https://benchmark.us)

In this episode of ‘On the House,’ we explore the impact of high-interest rates and challenges faced in 2023, emphasizing the importance of careful consideration before making housing decisions. Additionally, we delve into predictions for 2024, including forecasts for home sales, mortgage rates, and property values from industry experts.

Want to see if homeownership is right for you? Reach out to your local Benchmark branch to learn more. https://benchmark.us/

Legal and Compliance:

The information provided in this presentation is for general informational purposes only. The content shared here is not intended to be financial, legal, or professional advice specific to your situation. Mortgage regulations and requirements may vary, and the information discussed may not be applicable to your individual circumstances. Therefore, we recommend consulting with a qualified professional or contacting Ark-La-Tex Financial Services, LLC – NMLS #2143 directly for personalized advice tailored to your needs. Any reliance you place on information from this presentation is at your own risk.

By listening to this presentation, you acknowledge and agree that Ark-La-Tex Financial Services, LLC – NMLS #2143, its hosts, and guests are not responsible for any losses, damages, or liabilities that may arise from your reliance information presented here.

Ark-La-Tex Financial Services, LLC NMLS# 2143 (www.nmlsconsumeraccess.org). All loans subject to borrower qualifying. This is not a commitment to lend. Other restrictions may apply. (https://benchmark.us)

Benchmark, a leading mortgage lender since 1999, is proud to announce its accreditation as an Accredited Social Impact Lender (ASIL) by the National Association of Minority Mortgage Bankers of America (NAMMBA).

This accreditation is a testament to Benchmark’s commitment to providing quality mortgage services to all of its clients. Benchmark’s mission is to make homeownership accessible to everyone, and this accreditation is a major milestone in achieving that goal.

“We are thrilled to be recognized by NAMMBA as a Social Impact Lender,” said Benchmark CEO, Brian McKinney. “At Benchmark, we strive to provide our clients with the best possible service and this accreditation is proof of our commitment to our mission.”

NAMMBA is a national organization dedicated to promoting diversity and inclusion in the mortgage industry. The ASIL accreditation is a rigorous process that requires lenders to demonstrate their commitment to social impact lending.

“We are proud to have Benchmark join our ranks of ASIL lenders,” said NAMMBA President, Tony Thompson. “Benchmark’s commitment to providing quality services to all of its clients is a testament to their dedication to their mission.”

Benchmark is committed to providing its clients with the best possible service and this accreditation is a major milestone in achieving that goal. With this accreditation, Benchmark is now better equipped to serve its clients and help them achieve their goals of homeownership.

For more information about Benchmark and its services, please visit benchmark.us.

Benchmark could just be another mortgage lender, but we’re not. Sure, every company has their ‘core values’, but there is something tangible and special about ours.

Our core values didn’t exist until after they were identified in the soul of the company years after it was established. These values not only inform how we do things, they defined what was already at work. They support an existing culture, rather than being the rules for mandating it. First and foremost, Benchmark is about relationships.

We recognize, and experience, the reality that it is people just like you who make what we do worthwhile. It’s not about money, fame, or pride; in the end, it’s about having the privilege to serve so many people in financing their dreams, while care for their future.

There are many client stories that remind us why we do what we do, and validate our mission. Stories like this one from our branch in Imperial, CA.

Good evening team, I wanted to thank you again for an incredible job getting the Rosales home for Christmas. They were homeless for 6 months, and living in a friend’s room with 2 kids.

We knew we could close for New Year’s but for Christmas we needed a miracle, and today when I give them the news that the house was recorded under their name, the first thing they told me was,

“Please thank everyone on your team because we knew we needed a Miracle and that Miracle is Benchmark. For the last 3 days every time I give Mom an update she will cry and I kept telling her don’t cry because you will make me cry.”

I was lucky to be present when they got the keys, and seeing her kids choosing their rooms and wanting to move all their furniture from storage tomorrow was the greatest gift I could have received as a Loan Officer.

My client knows I’m the face of Benchmark, but without any of you this will never be possible.

At Benchmark, we are committed to listening to your goals and setting you up for future success. To learn more, Contact your local Benchmark branch. Contact us today for personalized information. Call me yourself or request a call from me. WeI would be honored to provide you with our famous excellent service.

A Home Equity Line of Credit (HELOC) is an easy way to borrow money using your home’s value as collateral. Let’s look into how a HELOC works and whether this option is right for you.

A home equity line of credit (HELOC) works much like a credit card. With money drawn from a HELOC, you can pay for things like home remodeling/repair fees, credit card debts, or even save it for rainy day funds.

A HELOC’s interest rates can be significantly lower than a credit cards

How Much Can You Borrow with a HELOC?

The first step in deciding if a HELOC is right for you is knowing whether you have enough home equity to qualify. This will also determine the amount of the credit line that you’re eligible for.

Your home equity is the difference between your home’s appraised value and your mortgage balance (assuming you have an existing mortgage).

Example: HELOC for a home worth $500,000

if your home is worth $500,000 and you have 50% equity, you may be able to borrow as much as $150,000 in a Home Equity Line of Credit (HELOC).

Let’s break that down.

If your home is worth $500,000 and you owe $250,000, your equity is 50%.

$500,000 – $250,000 = $250,000

If your home is worth $500,000 and you don’t have a mortgage, your equity is 100% ($500,000 – 0 = $500,000).

To estimate your possible HELOC credit limit, calculate your combined loan-to-value ratio (CLTV ratio, or your line of credit relative to your home equity). Most HELOC lenders allow a CLTV of at least 80% on your main home, sometimes higher.

To estimate, multiply your home’s appraisal value by 0.8. This is approximately how much money lenders may let you borrow against your home. With a home value of $500,000, it comes to $400,000.

$500,000 x 0.80 = $400,000

Then, subtract the amount you still owe on your existing home loan. For our example, let’s estimate that to be $250,000.

$400,000 – $250,000 = $150,000 credit limit for our example HELOC.

So, How Does a HELOC Work?

A HELOC is a revolving line of credit with a variable interest rate, like a credit card. It also has a fixed term and a defined repayment period, like a mortgage.

A credit card’s credit limit is based on your household income and credit score. You can spend as much, up to the credit limit, or as little as you want in each billing cycle. When you get your statement, you have to make at least the minimum monthly payment, but you can choose to repay the entire statement balance if you don’t want to accrue interest. When your payment is processed, your available credit increases by the amount of your payment that went toward the balance. If a portion of your payment is going to interest, this portion will not contribute to your available credit.

A HELOC is similar, but your credit limit is also based on how much equity you have in your home. Additionally, a HELOC has two periods:

First, there is a draw period, typically several years, during which you can borrow up to your credit limit and make interest-only payments.

Then, there is a repayment period, generally several more years, when you can no longer borrow money but must repay your outstanding balance with interest.

What are the steps to get a HELOC?

Apply with a Benchmark online, in person, or over the phone.

You will be asked to submit supporting documents including photo ID, paystubs, tax returns, proof of assets, bank statements, current mortgage details, and other financial information

If approved, Benchmark will issue an initial, conditional approval

Benchmark will order and schedule an appraisal of your home.

Our underwriters will check your application and make sure everything’s in order

Your final approval will be sent by your underwriter

Close the loan and receive funding. Since a HELOC is not a lump sum loan, you’ll receive a special account or card allowing you to access your HELOC as needed

What else should you know to decide if a HELOC might be a good choice for you?

We recognize that not every loan product is right for everyone. There are a few more things you should know about HELOCs.

Like most credit, the better your credit score and credit history, the higher the chances are that you will be approved.

A HELOC is a very low cost way to borrow money, and can be an attractive option if you do not have a substantial amount in savings, and are in need due to a crisis or economic downturn.

You can use a HELOC to pay for almost anything, and funds are easily accessible once open.

If you feel burdened with credit card debt, and you’re looking for a way to save on interest, a HELOC could be a great tool.

Curious to learn more?

At Benchmark, we are committed to listening to your goals and setting you up for future success. To learn more, Contact your local Benchmark branch. Contact us today for personalized information. Call me yourself or request a call from me. WeI would be honored to provide you with our famous excellent service.

The VA loan is one of the most powerful home buying tools available to those who qualify. A few benefits of the VA home loan are an option for ZERO down payment, no Private Mortgage Insurance, and lenient credit qualifications.

There are specific criteria to qualify for the VA home loan, one of which is the Minimum Service Requirement. This is essentially a baseline for service qualifications.

The Minimum Service Requirements for The Army, Navy, Air Force, & The Marine Corps:

Served 90 consecutive days of active service during wartime.

Served 181 days of active service during peacetime.

Recently, the VA has revised their qualifications for those who serve and have served in the National Guard, which has opened the VA loan to thousands of National Guard members.

National Guard updated VA Loan qualifications are as follows:

If you’ve served for at least 90 days (minimum 30 consecutive days) of active duty under Title 32 orders, you meet the minimum service requirement.

Over recent years, thousands of National Guard members were activated under Title 32 Orders, meaning many of them are eligible for a VA Home Loan.

Have you served or are currently serving in the National Guard? Reach out to one of our branches today to learn about the VA home loan and find out if you are eligible today!

Get Your COE!

At Benchmark, we are dedicated to serving veteran clients and providing them with a world class home buying experience. We have changed the way VA lending is done. That is why Benchmark never quits.

Contact your local Benchmark branch. Contact us today for personalized information. Call me yourself or request a call from me. WeI would be honored to provide you with our famous excellent service for your new loan.

The resurgence of everything pumpkin spice means that fall is upon us once again. You are probably as excited to pull out that box of fall décor as we are. If you live in a building (a house, duplex, apartment, condo, etc..) then there are some other important tasks that should be added to your to-do list to make sure your home is well prepared for the change of season.

Have your furnace inspected

Don’t get left in the cold. Fall brings cooler temperatures, shorter days, and earlier sunsets. Ensure that your home stays nice and cozy by having your furnace inspected. Contact your preferred local HVAC company to get your furnace checked out and maintenance, if needed.

Clean your gutters

Gutters safely carry water from your roof away from your home’s foundation. Blocked gutters can prevent this water from flowing, causing damage to your home, so it is important to clear out any debris that has built up. You can hire someone to do this, or you can do it yourself. Consider getting gutter guards so that water will flow smoothly without your gutters getting clogged with leaves or other debris.

Properly insulate your home

Combat the drop in temperature by making sure your home is properly insulated. The most effective way to keep your home warm is to invest in extra insulation, and there are many different options that vary based on your type of home and specific layout. This can be pricey, but will save money on energy bills in the long run. You can also reduce heat loss by covering windows with blinds and curtains.

Check outdoor faucets

Make sure all outdoor faucets are turned off. It might be worth doing now, before winter, to avoid water freezing and bursting pipes. Don’t forget to use insulated covers for exterior water spigots.

Bring in outdoor items

Depending on the weather, it may be best to pack up outdoor furniture and other patio items that could get damaged. If you have a pool, it might be time to cover it so that it stays clean until next summer.

Following these tips can help you avoid common problems in the fall and winter. By making sure that your home is well prepared, you can relax and enjoy all that this season has to offer.

With mortgage interest rates at a level not seen for over a decade (see chart below), the question of whether to wait for interest rates to fall is creeping in. This is not unreasonable, however, it does beg the question.

Are rates actually high?

If you take a look at the chart below, you can get a pretty good idea. At first glance, you may be tempted to think, “With rates THIS high, they’re bound to come back down before too long.” You may think this looks like an economic blip; that things will calm down back to normal soon.

But a longer view may give you a different perspective.

Looking over the past ten years means we are looking back on a housing market recovering from the 2008 crash (the conditions of which do not exist today). This is a short-term view; A view that includes a lot of market manipulation intended to encourage buying through various means, including keeping interest rates low.

To see more clearly, we need to take a look at a much longer time frame.

The longer view gives a sobering realization. Current rates do not appear to be high at all, in the long term. The reality is that the lower rates we’ve been experiencing are a strange occurrence, fueled by quantitative easing. The rising rates we see now are the result of a slight reversal of this practice. To better understand what this really means, take a look at the chart of the Federal Reserve’s Balance Sheet over the last 10 years below.

The Federal Reserve was buying investment securities (including mortgage debt securities) to help prop up the economy, and to bring mortgage interest rates down. The fact that the strategy worked is a clear sign that its reversal means that rates have, and will probably continue to drift back up to natural market levels. As we have discussed before, a rising interest rate means a rising cost of homeownership.

However, it’s clear that interest rates are not the only thing going up.

Inflation is a value killer

Inflation is on everyone’s minds as of writing. The Consumer Price Index shows a fairly sharp climb since the COVID-19 pandemic began, and the Federal Reserve’s increase in interest rates (not the same as mortgage interest rates) was intended to alleviate inflation. Oh, you want a chart to show inflation? See below.

The rising prices means that your money is worth less. Everything costs more than it did, which can eat into what you can afford for a monthly mortgage payment. It may seem like a good idea to wait: for your money to be worth more, for the economy to stabilize, and for mortgage interest rates to return to their senses.

As discussed previously, however, there is no solid basis for anticipating mortgage rates to come down any time soon, if at all. If this is true, though, does it even make sense to buy a home? Is real estate really the right place to put your money if the cost of living goes up?

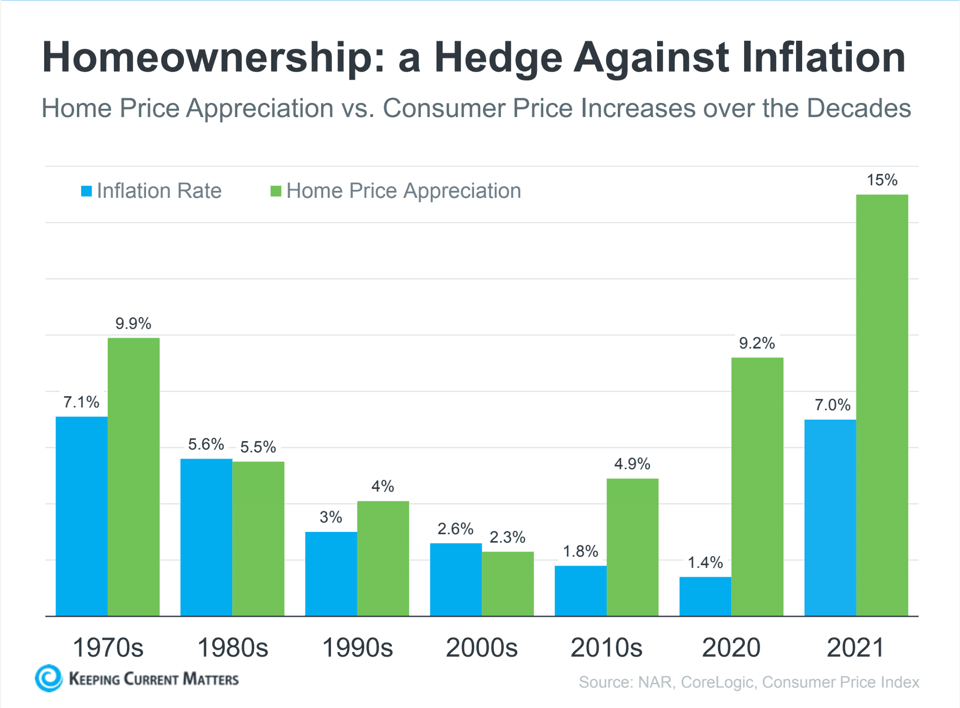

Rising prices mean cash held in hand is losing value, while investments that rise with it are, at the very least, holding value.

“Real estate is one of the time-honored inflation hedges. It’s a tangible asset, and those tend to hold their value when inflation reigns, unlike paper assets. More specifically, as prices rise, so do property values.”

Mark Cussen, Financial writer at Investopedia

Higher cost (rates) means less competition

We have seen a cooling of demand in the housing market since rates have started rising. The sellers’ market has become more equitable, favoring buyers in many locations. There have been fewer multiple-offer scenarios, and even when there are multiple-offers, there have been fewer offers to compete with.

If you live in a competitive market, Benchmark can give you an edge. If you don’t live in a competitive market, this could be your opportunity to get your offer accepted on the best possible terms. Again, this is what we do best. Contact us get more information about how you can win with Benchmark.

Housing prices tend to climb

The financial world is full of commonly repeated advice. Invest early and invest often. The best time to plant a tree is 20 years ago; the second best time is today. Add this one to the list: Buy now to buy more.

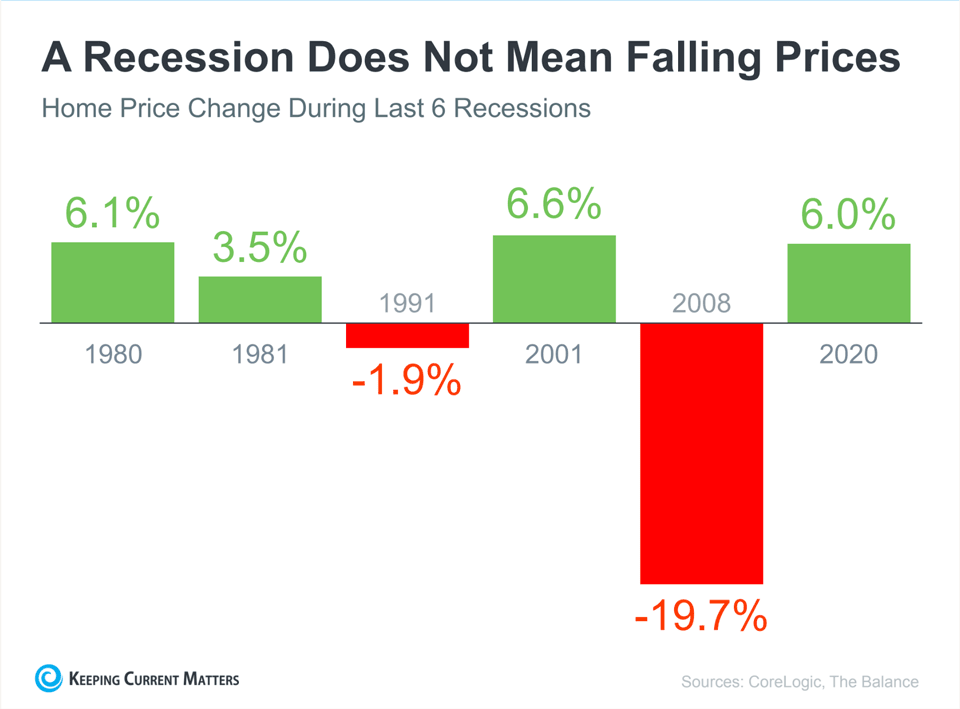

Even if we find ourselves in a recession, as some predict, this does not guarantee falling home prices. The exception being the notorious 2008 recession due to the collapse of real estate debt-based investment schemes, the conditions of which do not exist, and have not existed since.

There is no indication that they will come down any time soon. Even if you do suspect that rates will be reduced in the future, you should weigh the cost of waiting. Of course, you may be able to refinance at a lower rate in the future, while taking advantage of current home prices now.

Either way, your rent payment will become at least a partial investment into a physical asset you own. The principal portion of a mortgage payment directly reduces the amount you owe on your home. When you pay rent, the only equity you are building is your landlord’s.

The chart above is not plotting rent prices. The chart is plotting rent price inflation. See the dip caused by the COVID-19 pandemic starting early 2020? This isn’t really a dip; it’s just a reduction in the annual inflation rate of rent prices. Inflation never reversed within the last decade.

How do you escape the squeeze?

It would do no good to lie to you and tell you that there is an easy way out of the rising cost of housing. We have published a short list on How to Get Ahead When You Can’t Get the House You Want, but the wisest words I’ve ever read on housing were these: “Welcome to California. Buy a house immediately.” This is less about California, and more about how to live with rising housing prices. This was advice given to someone who moved there for a job in the tech industry. The advice holds true now: the sooner you buy, the better your chances of being able to buy.

If you think you might want to become a homeowner, I encourage you to contact us. Even if you think you cannot afford a home yet, or if you don’t know what you need to do to get started, we specialize in helping people just like you achieve the American dream of homeownership. Benchmark has been helping people get into their own home since 1999, and we’ve learned a few things along the way.

Contact your local Benchmark branch. Contact us today for personalized information. Call me yourself or request a call from me. WeI would be honored to provide you with our famous excellent service for your new loan.